Behind China’s Phosphate Fertilizer Export Ban: Strategic Resources, Food Security, and the Circular Economy

Phosphorus policy

14 March 2026 at 12:00

Phosphorus policy

14 March 2026 at 12:00

As China enters the critical spring planting season of 2026, demand for fertilizers is rapidly increasing across the country. At this key moment, on March 14, the General Administration of Customs issued an urgent notice suspending all export declarations for phosphate fertilizers and phosphate-containing fertilizers. The ban covers monoammonium phosphate (MAP), diammonium phosphate (DAP), superphosphate, and compound fertilizers. No new export declarations are accepted after March 14, and shipments already declared but not yet cleared are also blocked. The policy will remain in place until August 31, effectively enforcing a “zero-export” regime. Non-agricultural phosphate products—such as purified phosphoric acid, feed-grade phosphates (DCP/MCP), yellow phosphorus, and iron phosphate—are not affected and can still be exported.

This move is not a sudden tightening, but the result of multiple pressures converging. International phosphate fertilizer prices are currently 20%–30% higher than domestic levels, creating strong incentives for exports. At the same time, China is in the peak of its spring planting season, when domestic demand is already high. Upstream costs, including sulfur and phosphate rock, have also been rising, further tightening supply conditions. Under such circumstances, allowing exports could quickly lead to domestic shortages and price volatility, directly affecting agricultural production costs. By controlling exports at the declaration stage and enforcing the policy without exceptions, authorities are intervening precisely at a moment of peak supply-demand tension.

At a broader level, the policy is primarily aimed at safeguarding agricultural stability. Phosphate fertilizers are essential inputs for crop production, and their availability directly affects planting costs and yield expectations. In a global context of increasing volatility in food markets, ensuring stable access to key agricultural inputs has become more critical. Temporarily restricting exports helps stabilize domestic supply and prices, providing greater certainty for farmers during the planting season. While short-term market reactions—such as stockpiling or tentative price increases—may occur, they are likely to remain contained under strong regulatory oversight.

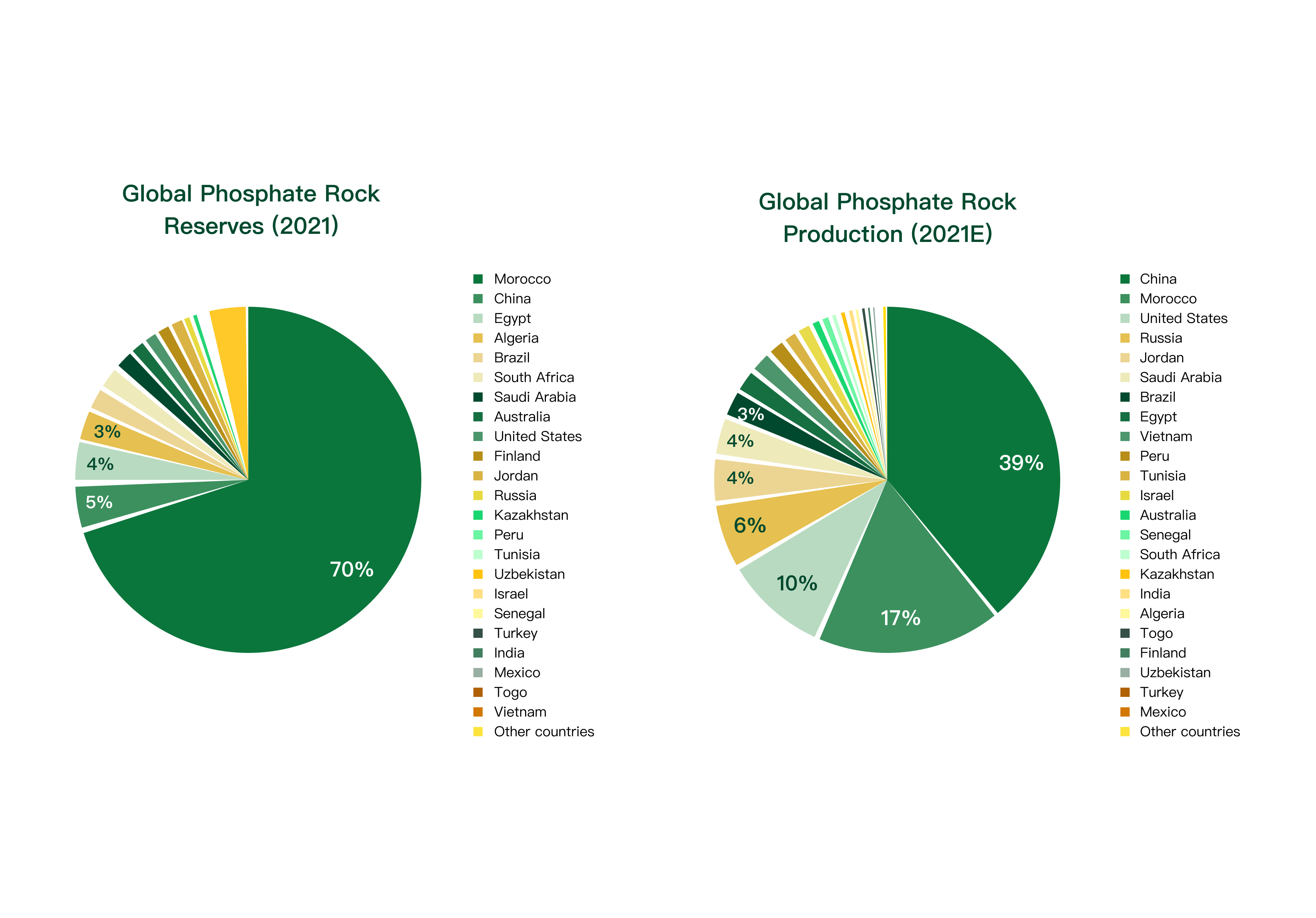

However, the policy cannot be fully understood as a short-term supply measure. A deeper logic is emerging: phosphorus is increasingly being treated as a strategic resource. As a non-renewable material, phosphate rock underpins not only agriculture but also sectors such as new energy and battery materials. China’s reserves are limited, with less than 30 years of supply at current extraction rates. At the same time, fertilizer use efficiency remains relatively low, with significant losses during application that ultimately end up in the environment. This combination of high consumption and low efficiency places pressure on both resource security and environmental sustainability.

In this context, restricting exports also creates space for structural adjustment. With external demand constrained, the industry is pushed to focus more on domestic efficiency and value optimization. This includes improving fertilizer use efficiency, reducing unnecessary inputs, and advancing the recycling of phosphorus from livestock waste, municipal sludge, and other sources. Technologies for phosphorus recovery and reuse are likely to gain greater attention. While these shifts may not produce immediate results, they will gradually influence technological priorities and investment directions across the sector.

From a global perspective, China’s role as a major phosphate fertilizer exporter means the ban will have clear spillover effects. A temporary withdrawal from the market is likely to tighten global supply, particularly for countries that rely heavily on imports. This could lead to increased price volatility and higher procurement risks in the short term. Over a longer horizon, it may also encourage countries to diversify supply sources or adjust fertilizer use patterns. In this sense, the policy highlights the growing importance of supply security for critical agricultural inputs and may contribute to a gradual reshaping of global phosphate trade dynamics.

It is also notable that the ban does not extend to industrial phosphate products such as yellow phosphorus and iron phosphate. This selective restriction reflects a more targeted policy approach: prioritizing agricultural needs while maintaining supply chains for higher value-added industrial sectors. At the same time, it signals a shift in how phosphorus resources are allocated, away from low-value consumption toward more strategic and industrial uses.

Source: AP Photo/Matias Delacroix